Crypto liquidity following Black Thursday

Black Thursday was largely due to the concurrent drop in traditional markets, caused by fears around the COVID-19 virus. The S&P 500 index fell by ~11% over the day, along with every other asset class except US Treasuries.

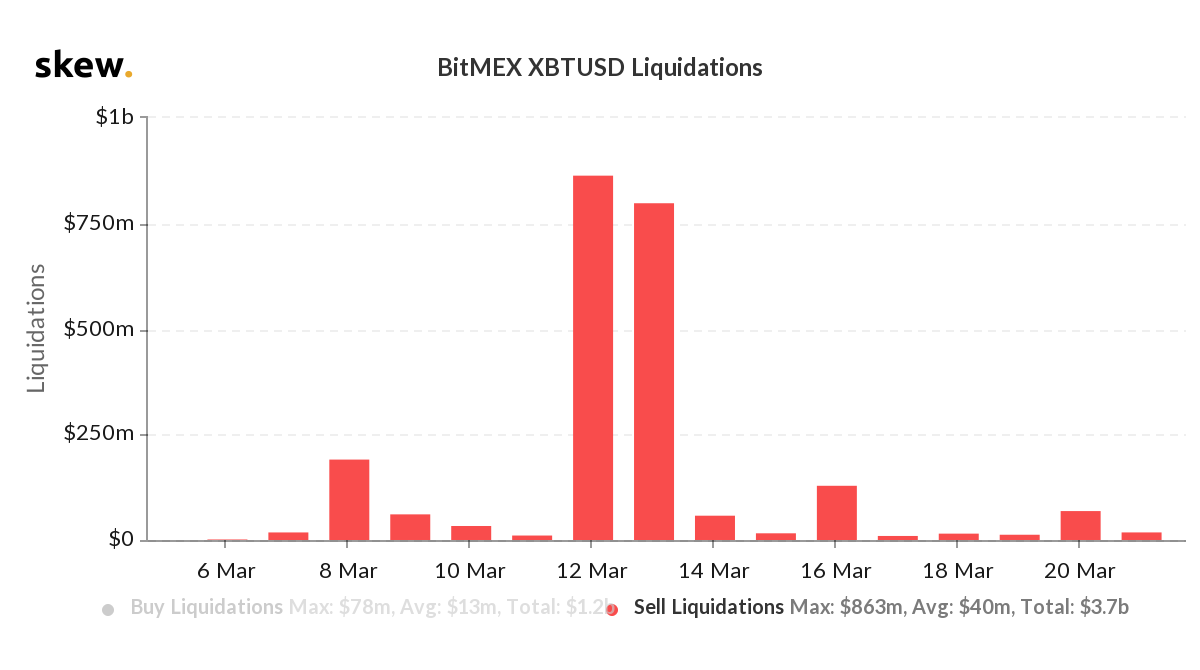

A key factor that exacerbated the severity of the crypto market crashes was a cascade of liquidations, otherwise known as a long squeeze, which occurred on derivative exchanges.

A long squeeze occurs when an asset's price dips below a position's liquidation level and/or traders stop-loss order, causing the long position to be sold, which pushes the spot price further down and causes the cycle to repeat. Over March 12th and 13th, over US$1.6T worth of long positions were liquidated on BitMEX alone.

Violent price movements coupled with huge volumes meant that market makers, who typically provide order book liquidity and profit from the bid-ask spread, were unable to stabilize the market.

A significant number of market makers and traders either withdrew their limit orders or were left holding positions underwater. This further exacerbated the price decline as liquidity almost completely dried up on derivative exchanges. The effect of the March 12th crash on order book liquidity has lingered on many of these exchanges. This is especially true for derivative exchanges.

Using Hsaka’s ‘Liquidity Bands’ indicator on TradingLite, we can gain insights into how various exchanges order books have fared following the crash. The liquidity bands plot the price where cumulative bids and asks are equal to a user-defined amount, which has been adjusted per exchange.

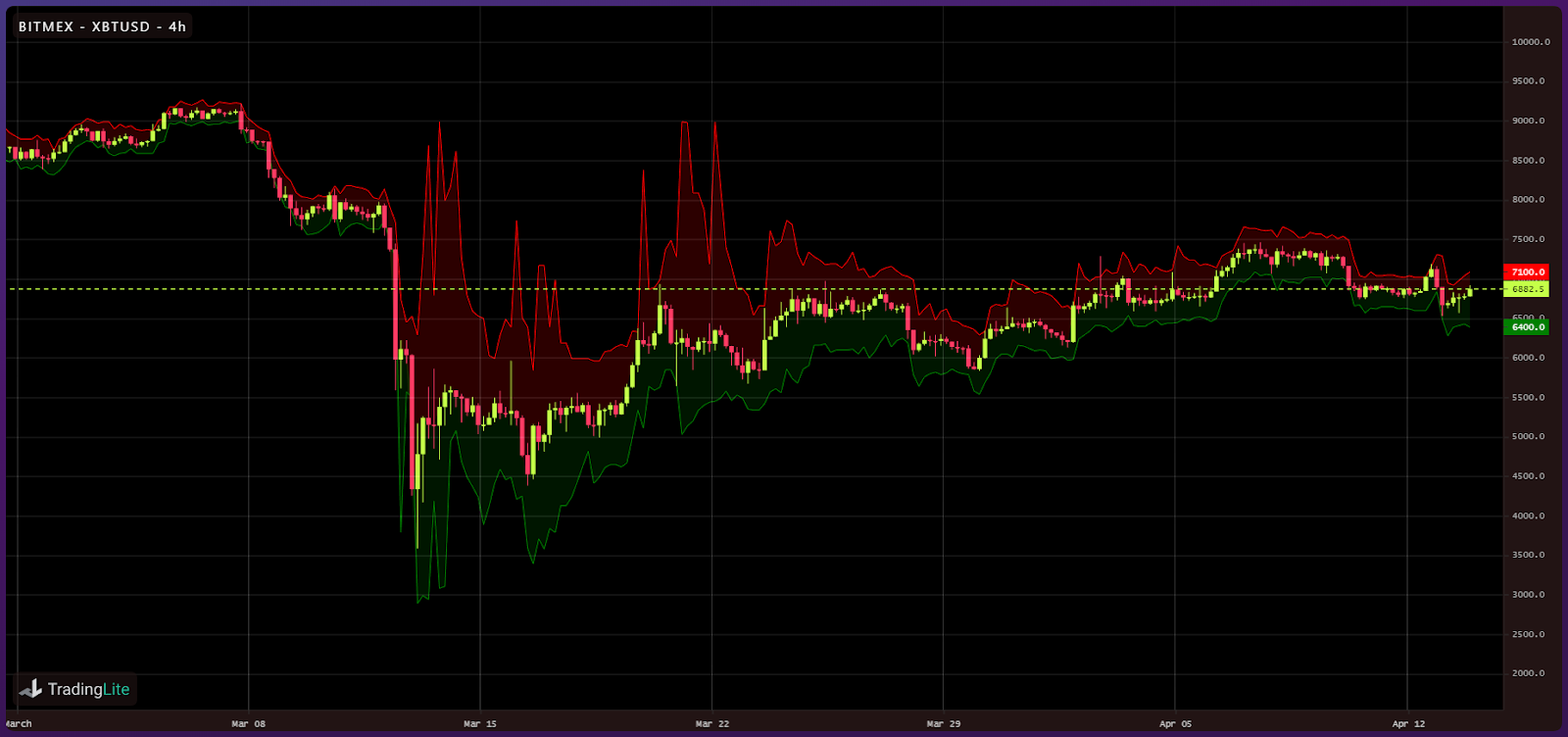

BitMEX BTC Liquidity Bands (US$50M each side)

The graph below shows the liquidity bands for US$50M worth of orders on either side of the Bitcoin (BTC) spot price on BitMEX. Prior to Black Thursday the bands were tight, indicating ample liquidity on both sides of the order book.

After the drop, however, the bands widened significantly, indicating that liquidity had dried up. As time went on, the bands began to tighten again. Whilst liquidity is still not what it was prior to the crash, it has recovered significantly since March 12th.

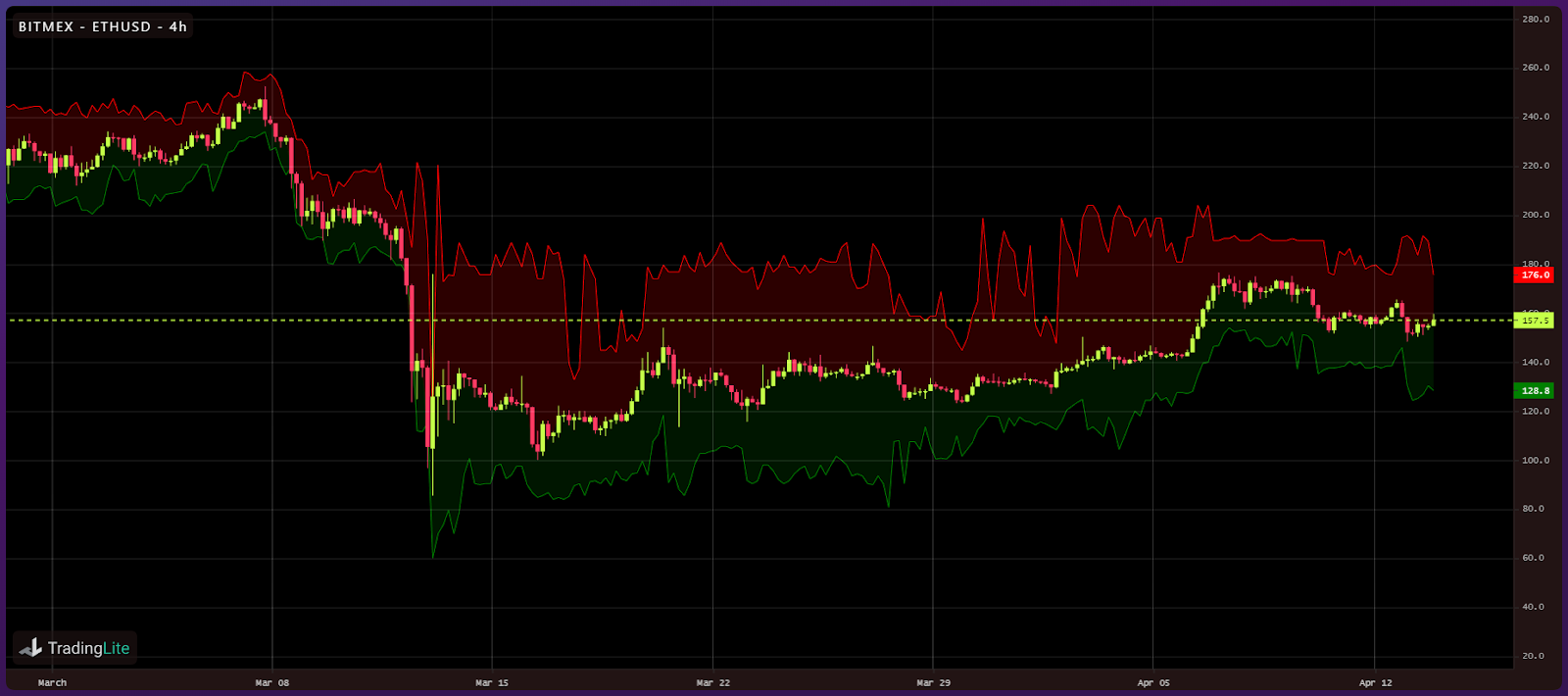

BitMEX ETH Liquidity Bands (US$10M each side)

The Ethereum (ETH) liquidity bands also widened significantly after the crash. However, order book liquidity is still quite sparse and has not recovered to the same extent that it has with BTC.

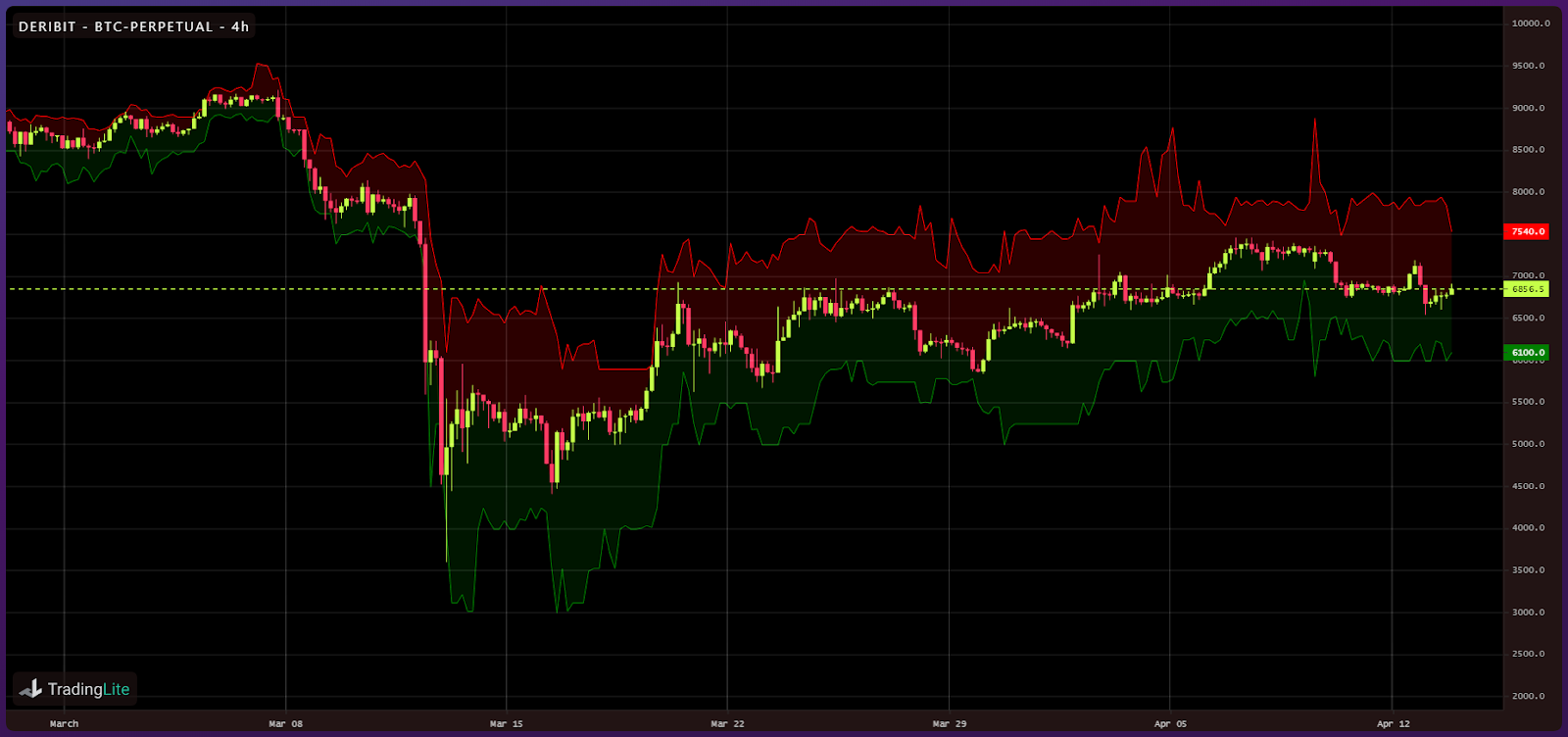

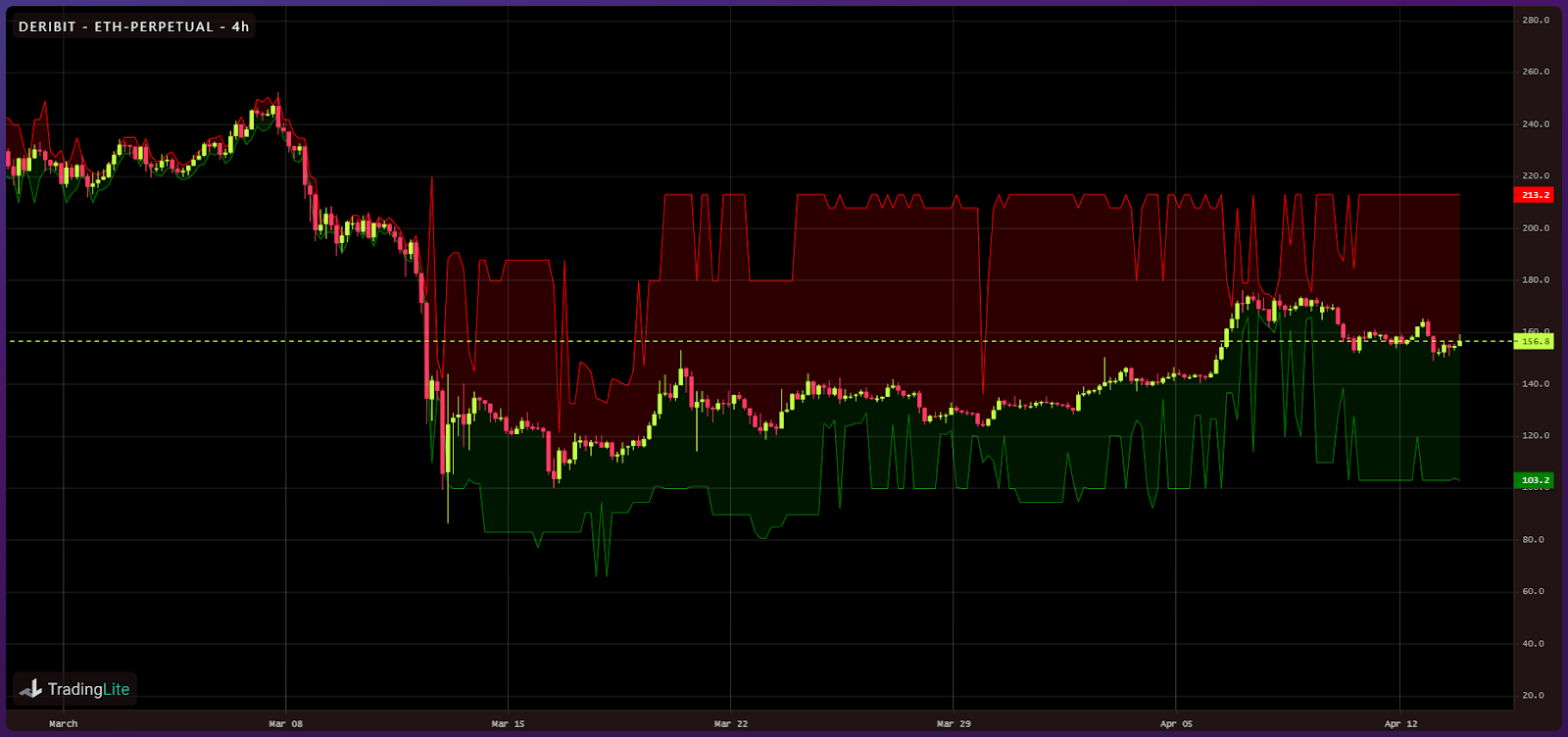

Deribit BTC Liquidity Bands (US$10M each side)

Switching to BTC on Deribit, the same pattern emerges of tight bands pre-crash and wide bands post-crash. Unlike BTC on BitMEX however, liquidity has remained low and has shown little signs of recovery. This indicates that market makers and traders have either stopped trading on Deribit or have significantly reduced their order sizes in response to increased market uncertainty.

Deribit ETH Liquidity Bands (US$2.5M each side)

As with BTC, ETH on Deribit has not had it’s pre-crash liquidity return, and in some cases the order book depth was worse in the weeks following the crash than immediately after.

Coinbase BTC Liquidity Bands (1k BTC each side)

Moving onto spot exchanges and starting with Coinbase, we can see that the liquidity band pattern that had emerged on the derivative exchanges appears absent with BTC. The opposite appears to be true: post-crash liquidity bands are tighter than pre-crash liquidity bands.

This is an interesting distinction that seems to indicate that market makers and traders are more willing to provide liquidity at current price levels on spot exchanges than on derivative exchanges. It’s important to note that volume on spot exchanges is denominated in the underlying asset (BTC or ETH), rather than in dollars like on derivative exchanges.

Coinbase ETH Liquidity Bands (10k ETH each side)

As with BTC on Coinbase, the same pattern holds true for ETH.

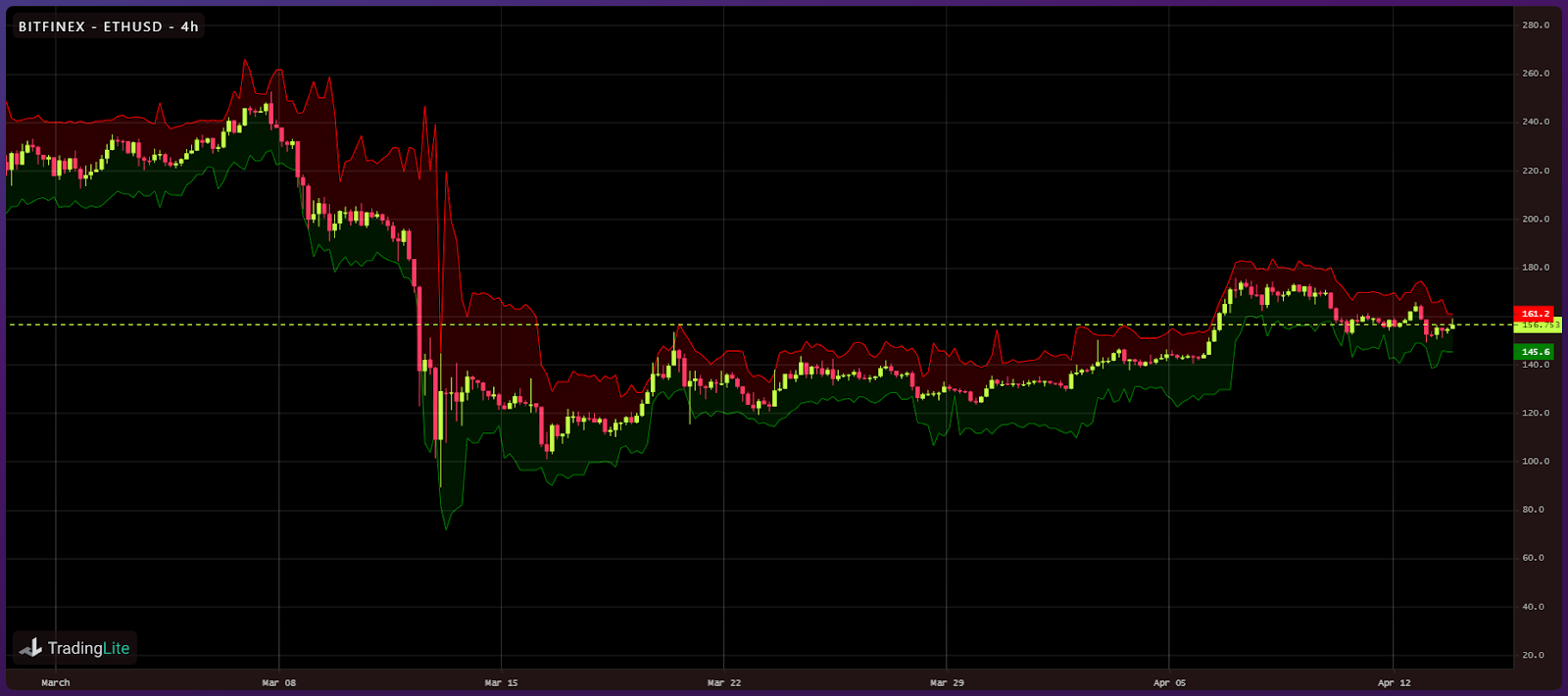

Bitfinex BTC Liquidity Bands (5k BTC)

Looking at BTC on Bitfinex, the liquidity band pattern is consistent with that of Coinbase’s. The defined band range of 5,000 BTC is also the highest of the spot exchanges, leading to slightly broader bands.

Bitfinex ETH Liquidity Bands (30k ETH)

ETH on Bitfinex has the same general pattern as Coinbase.

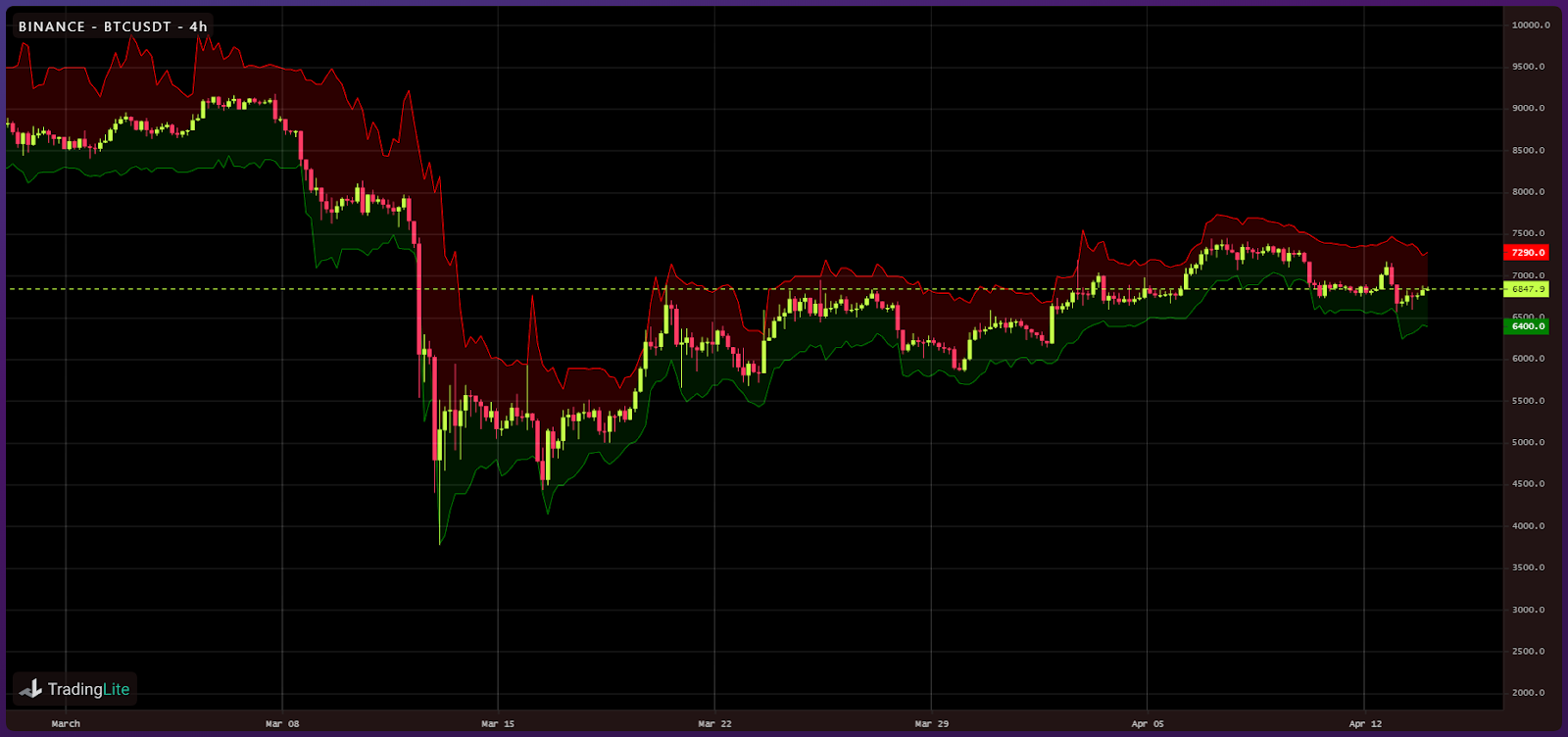

Binance BTC Liquidity Bands (3k BTC)

BTC on Binance has the same general pattern as the other spot exchanges.

Binance ETH Liquidity Bands (30k ETH)

ETH on Binance has the same general pattern as the other spot exchanges.

In summary, liquidity appears to be returning to BitMEX, but so far not Deribit. In contrast, spot exchanges have greater liquidity than before the crash. This is an interesting distinction that seems to indicate that market makers and traders are more willing to provide liquidity at current price levels on spot exchanges than on derivative exchanges. It could also be due to holders ‘cashing out’ or ‘new money’ flowing into the market.

The widening of the liquidity bands on derivative exchanges during the crash as opposed to the relatively normal bands on spot exchanges also indicates that the move down was largely driven by trading on the derivatives exchanges.

OhNoCrypto

via https://www.ohnocrypto.com

Bryce Galbraith, Khareem Sudlow