Ethereum Price Analysis - Development outpaces fundamental metrics

Ethereum (ETH) is a distributed ledger and decentralized computing platform with smart contract capabilities. The crypto asset is currently second on the BraveNewCoin market cap table, with a market cap of US$14.47 billion and US$1.79 billion in trade volume over the past 24 hours.

The ETH project was proposed by Vitalik Buterin in 2013. Other co-founders include Anthony Di Iorio, Charles Hoskinson, Mihai Alisie, Amir Chetrit, Joseph Lubin, Gavin Wood, and Jeffrey Wilcke.

An Initial Coin Offering (ICO) followed in 2014. The ICO raised nearly US$16 million, with each token selling for US$0.31. The ETH ICO would eventually become one of the most profitable in history.

The network mainnet went live in July 2015 with 72 million pre-mined coins, which currently accounts for 66.5% of the circulating supply. On Christmas day, Wilcke sent 92,000 ETH, US$11.5 million, to the Kraken exchange, presumably to sell. ETH was launched with no vesting schedule or lock-in period for coins.

Thus far, protocol upgrade milestones have included; Olympic in May 2015, Frontier in July 2015, Homestead in March 2016, Metropolis Part 1: Byzantium in October 2017, Metropolis Part 2: Constantinople in February 2019, and Istanbul in December 2019.

Ethereum is upgraded through a series of Ethereum Improvement Protocols (EIPs), which are then bundled into each hard fork. The Github repository for EIPs has been extremely active since January 2019.

In total, almost 1,000 developers have contributed a cumulative 28,000 commits to the ETH project in the past year, across 218 Github repos. Most of the commits over the past year have occurred in the Solidity repo, the programming language used to write smart contracts on Ethereum.

An adjacent protocol overhaul, Serenity, is currently in development and includes a full

rewrite and redesign, which will result in Ethereum 2.0. Phase zero of the herculean task could launch as early as January 2020. Both versions of ETH will exist concurrently for some time before a migration is completed. Danny Ryan, Justin Drake, and Vitalik Buterin have the most commits in the ETH 2.0 repo.

Overall, ETH related repos have had more commits than any other crypto project over the past year. This week, Buterin also released an alternative proposal for merging ETH 1.0 to ETH 2.0 on an accelerated schedule and less re-architecturing.

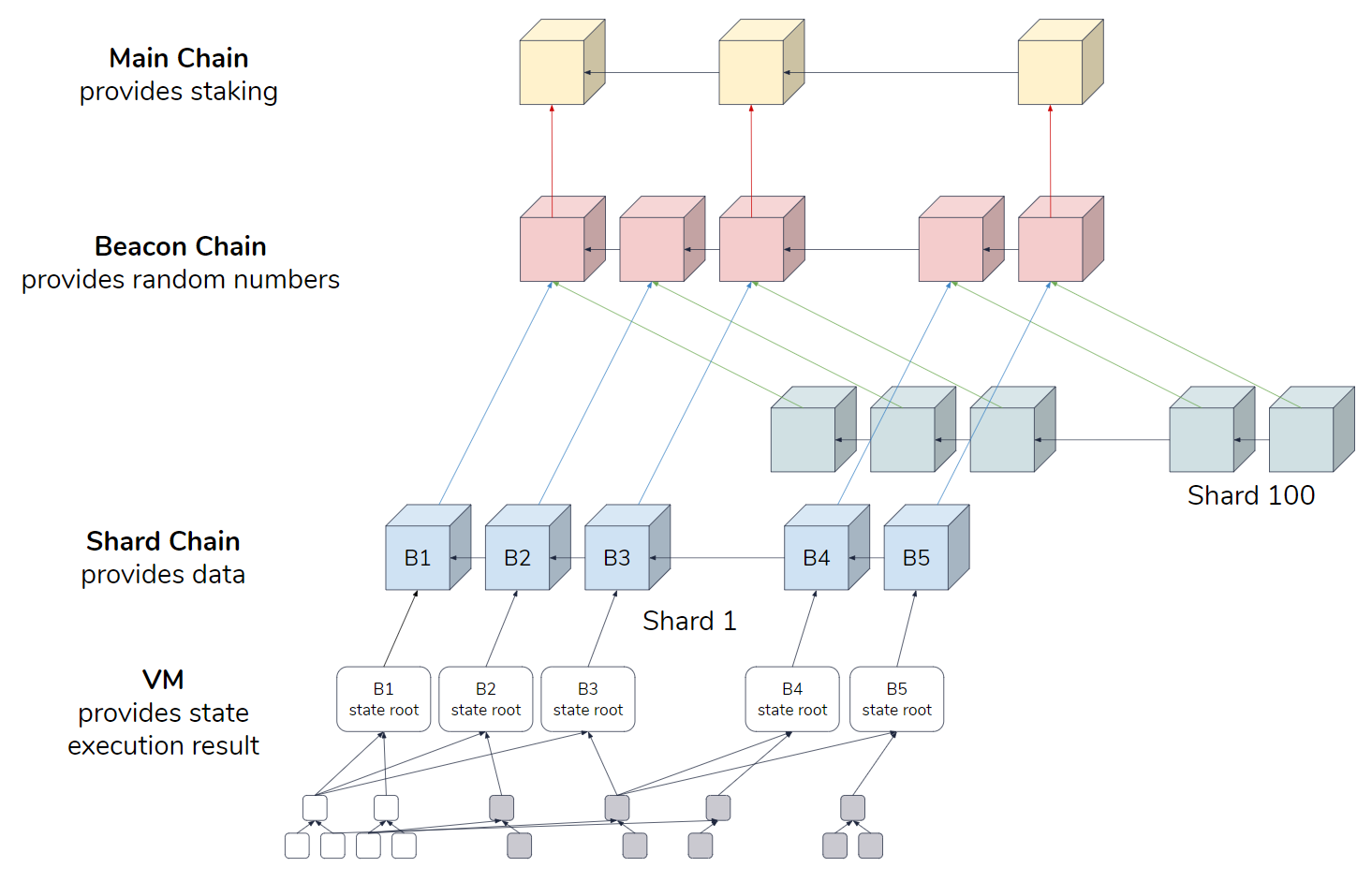

ETH 2.0 includes Sharding and Casper, which will drastically alter the network. Sharding refers to a scaling solution for horizontally partitioning data within a database. The full implementation of Casper, slated for release in 2022, will remove Proof of Work (PoW) from the network and replace it with Proof of Stake (PoS), with a block reward at 0.22 ETH/block. Currently, there are no plans to cap the total amount of ETH created.

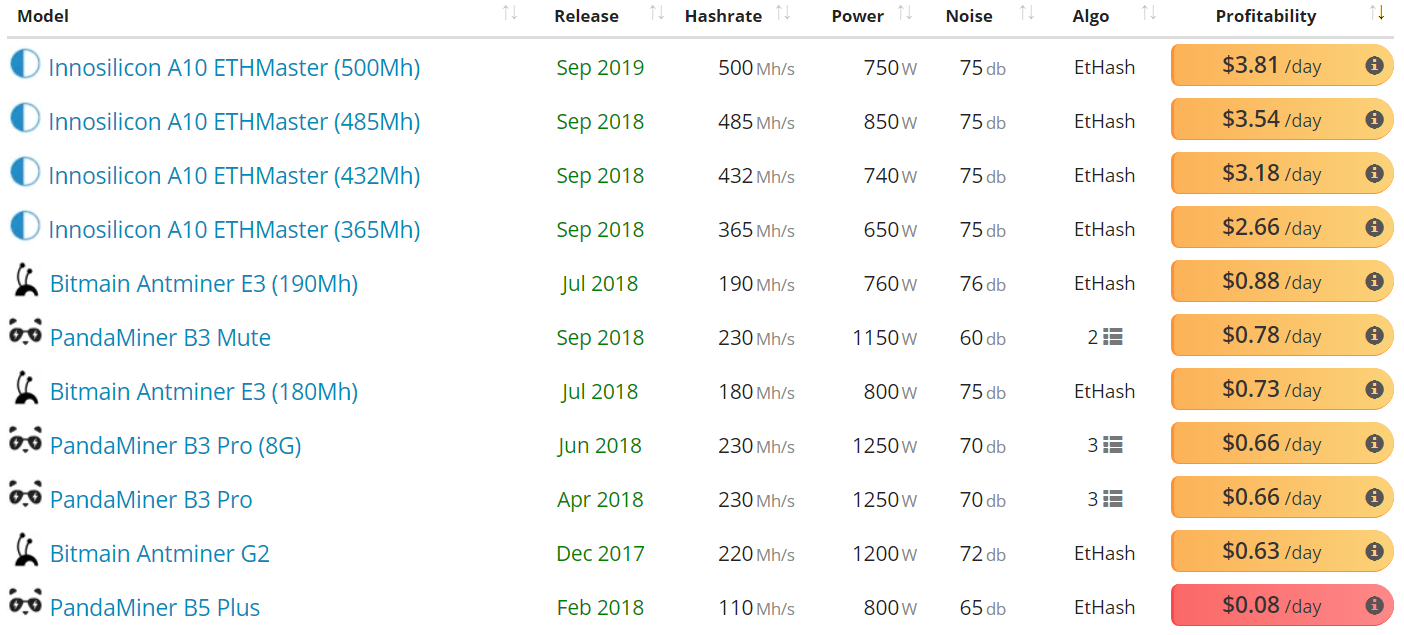

While the network is still PoW based, Programmatic PoW (EIP 1057) will likely be implemented in Istanbul, pending a successful audit. ProgPoW is designed to reduce ASIC mining on a network by increasing the efficiency of GPU and FPGA mining. Innosilicon and Bitmain both currently have three ASIC miners available for the EtHash algorithm, while a new ASIC mining chip from a third mining company, Linzhi, was released in October 2019.

If implemented, EIP 1057 will make all current Ethash ASICs unable to mine the chain. Those using Ethash ASICs may choose to continue mining the pre-fork chain. Another possibility is that ASICs will be used to mine the Ethereum Classic (ETC) chain, which also uses the Ethash algorithm. In any case, the goal of decreasing ASIC use on the ETH chain will be successful, although likely temporary. At US$0.05/KWh, all currently available Ethash ASICs are profitable. Mining profitability remains near all-time lows and If ETH prices fall significantly, hash rate will likely follow suit.

Hash rate (solid line, chart below) has declined steadily and slowly since the end of September, reaching for multi-month lows. Difficulty (dashed line, chart below) has risen steadily since April 2019, becoming disconnected from hash rate in October. This rise in difficulty despite a fall in hash rate is coded into Ethereum and known as an Ice Age, or difficulty bomb, which has activated twice before on Ethereum, once in 2017 and once in late 2018.

The most recent Ice Age was meant to serve as a transition from ETH 1.0 to ETH 2.0 and phase out PoW mining completely. However, because ETH 2.0 is not currently ready, the Ice Age will be pushed back another four million blocks, to block 13.2 million. Delaying the Ice Age will require a hard fork, currently scheduled for block 9.2 million, or around January 2nd.

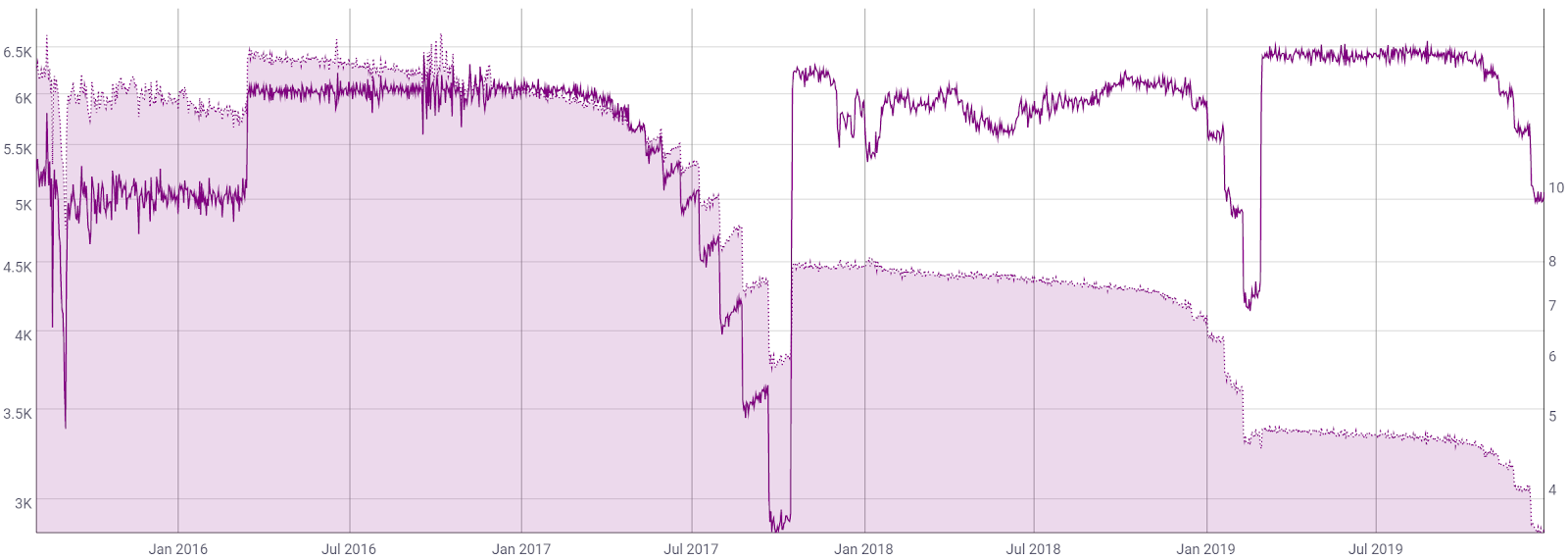

Due to falling hash rate and rising difficulty, the average block time is currently 17 seconds, up four seconds from the historic record lows earlier this year. The block count per day (line, chart below) has therefore decreased sharply as well. There are over 109 million ETH in circulation with inflation per annum currently at 3.51% (fill, chart below), which represents an all-time low. Despite increasing block times, pending transactions are holding near 40,000, with only a few smart contracts accounting for most of the transactions.

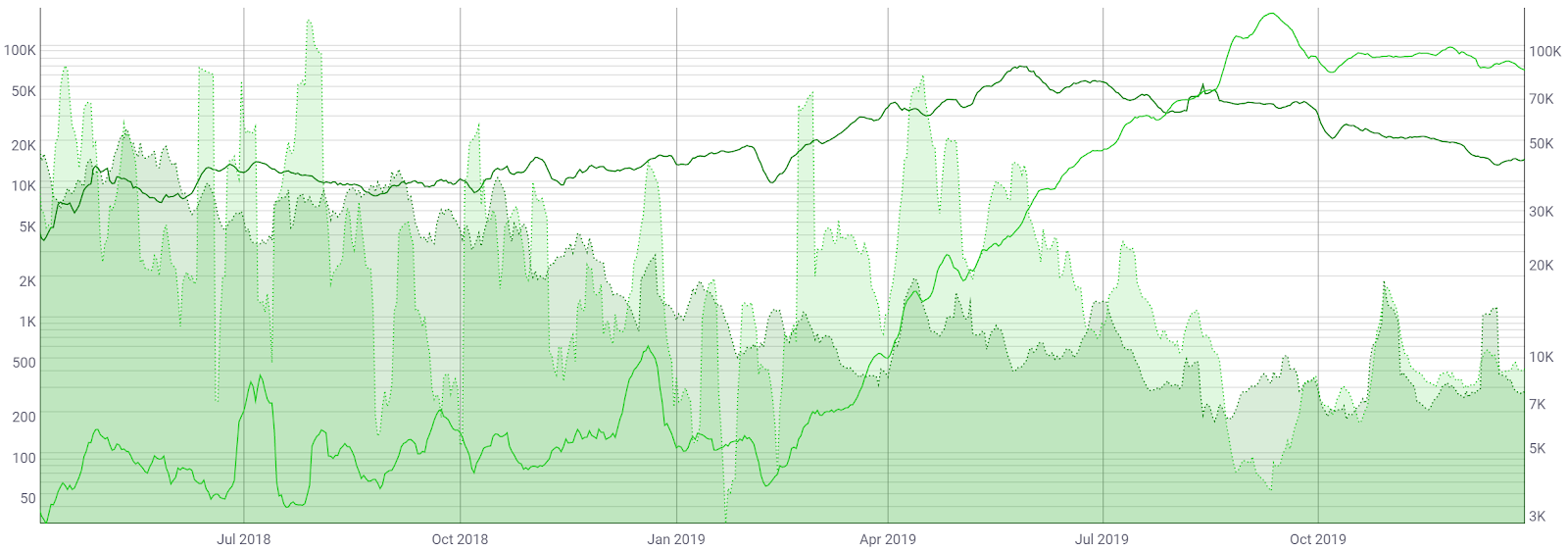

Tether (USDT) was originally issued on the OMNI chain in 2015, but has been aggressively swapped to an ERC-20 token over the past few months. In total, nearly 50% of all circulating USDT is now on the ETH chain. ERC-20 transfers are both cheaper and faster than OMNI transfers, thus many exchanges have added the option for ERC-20 USDT in recent months. ERC-20 USDT transactions per day (light green line, chart below) and average transaction values (light green fill, chart below) have quickly surpassed OMNI transactions per day (dark green line, chart below) and average transaction values (dark green fill, chart below).

The Ethereum network currently has 6,973 active network nodes, 33% of which are located in the United States and 40% of these nodes are running through Amazon Web Services. Due to the somewhat cumbersome hardware and time requirements of running a node, many of these nodes are run by Infura, or similar node servicers, who provide access to the network for developers. These services have become increasingly important as the blockchain continues to grow.

Nodes have several sync modes, with fast sync requiring approximately 234 GB of storage and a full archival node requiring nearly 3.5 TB of storage. To contrast, a Bitcoin full node requires just under 300 GB of storage.

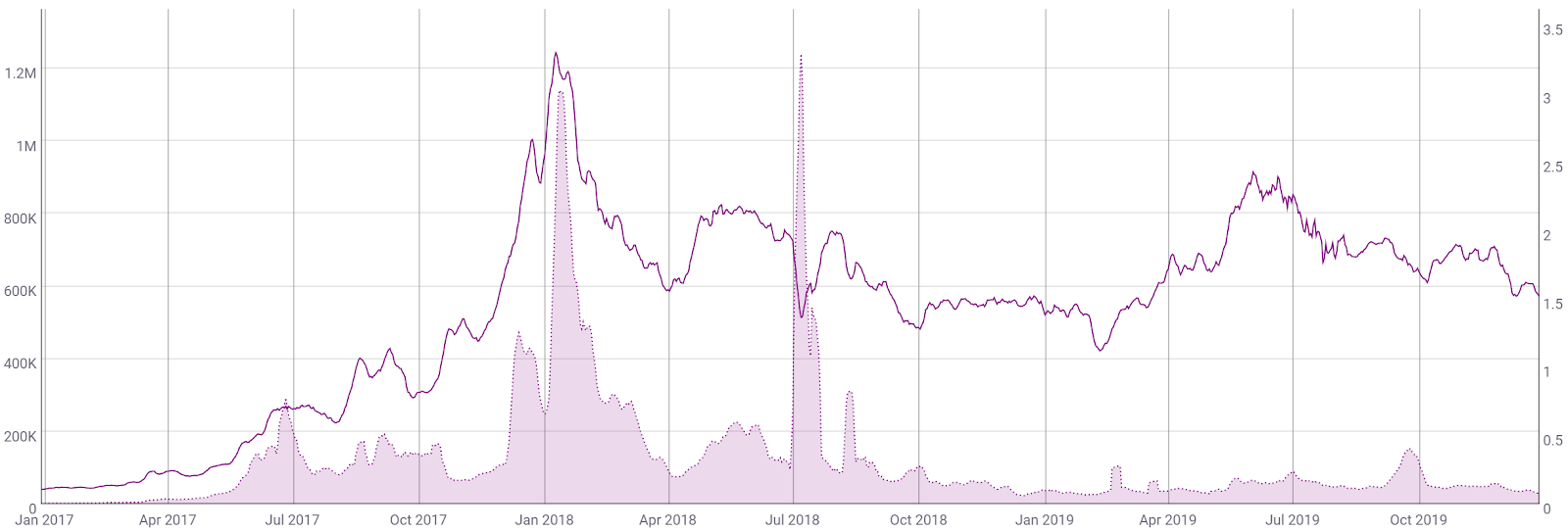

The number of on-chain transactions per day (line, chart below) has ranged from 650,000 to 750,000 since July but have now reach multi-month lows. This remains up from a yearly low of 430,000 in February, but down from the record high of 1.24 million on January 9th, 2018.

The average transaction fee (fill, chart below) is currently US$0.0795, down from over US$0.40 in late September. On February 19th and March 18th, the average transaction fee spiked to US$1.22 and US$0.63 respectively. Fees had been rising, despite declining transactions per day, because of a lack of efficient scaling methods. In September, miners voted to increase gas limits by 25%. Overall, fees are lower than during much of 2018.

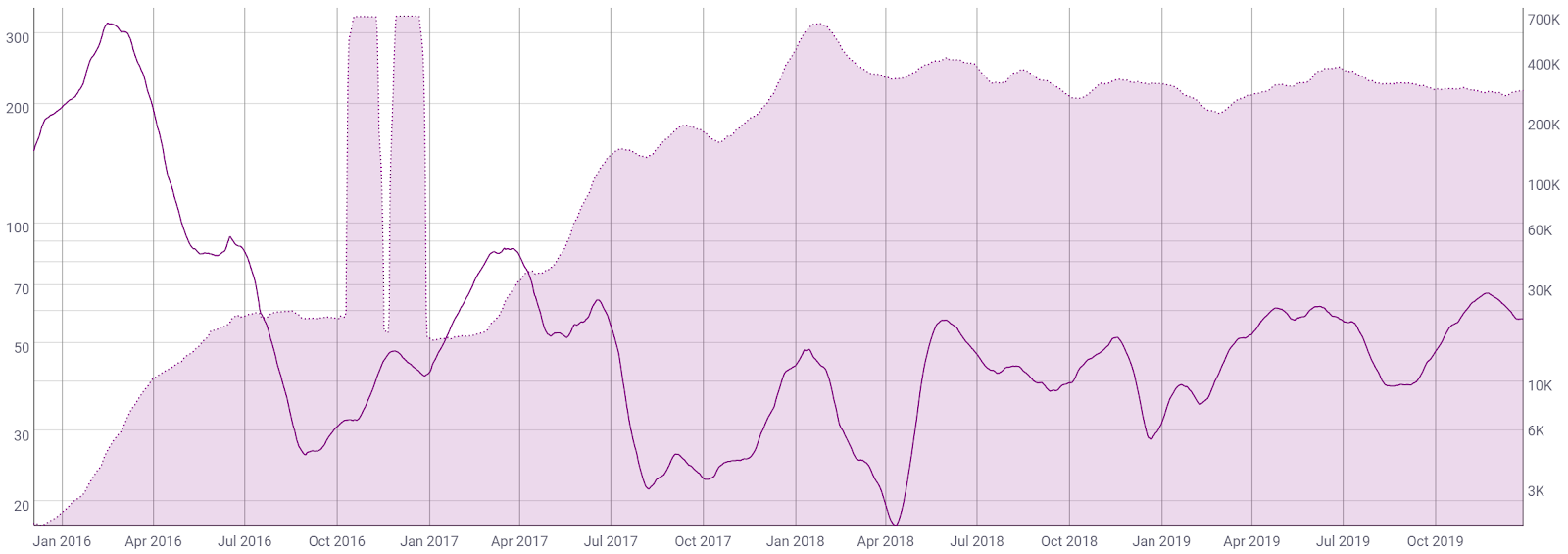

The 30-day network value to estimated on-chain daily transactions (NVT) ratio (line, chart below) has ranged from 30 - 66 since March 2018, and is currently 57. A clear uptrend in NVT suggests a coin is overvalued based on its economic activity and utility, which should be seen as a bearish price indicator, whereas a downtrend in NVT suggests the opposite. An NVT holding below 30 would likely signify bullish market conditions, as was the case from April 2017 to May 2018.

Monthly active addresses (MAAs) have continued to decline since late June and are currently near 280,000 (fill, chart below). MAAs are up from a yearly low of 192,000 in February, but down from an all-time high of nearly 610,000 in January 2018. Overall, MAAs remain above levels seen throughout 2017 and earlier. Unique addresses continue to grow at a rapid rate, and are nearly 80.7 million (not shown). However, addresses can only be added to the network, and are never deleted.

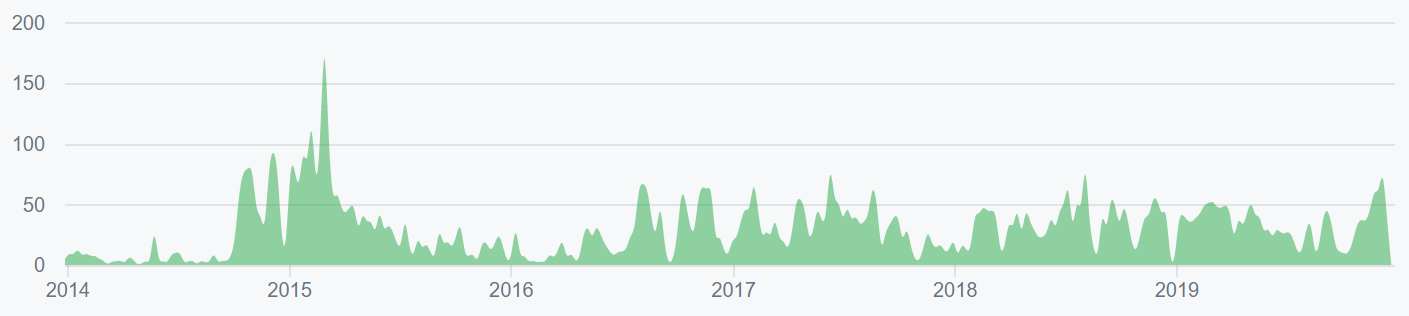

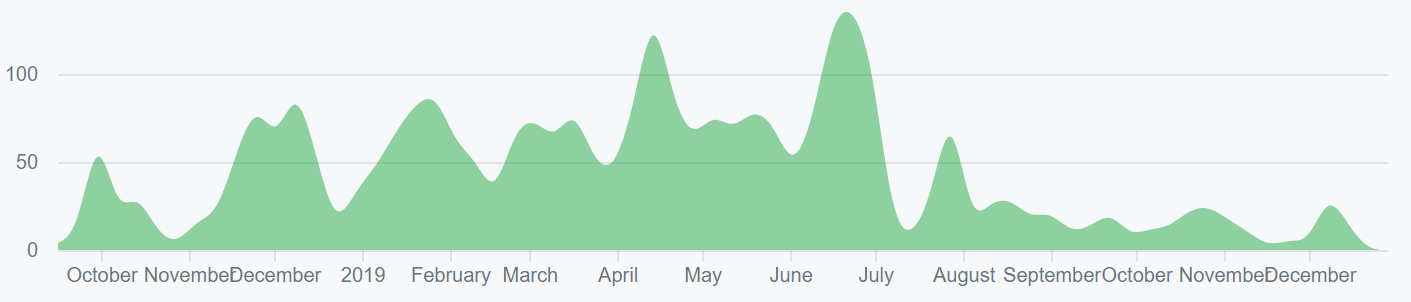

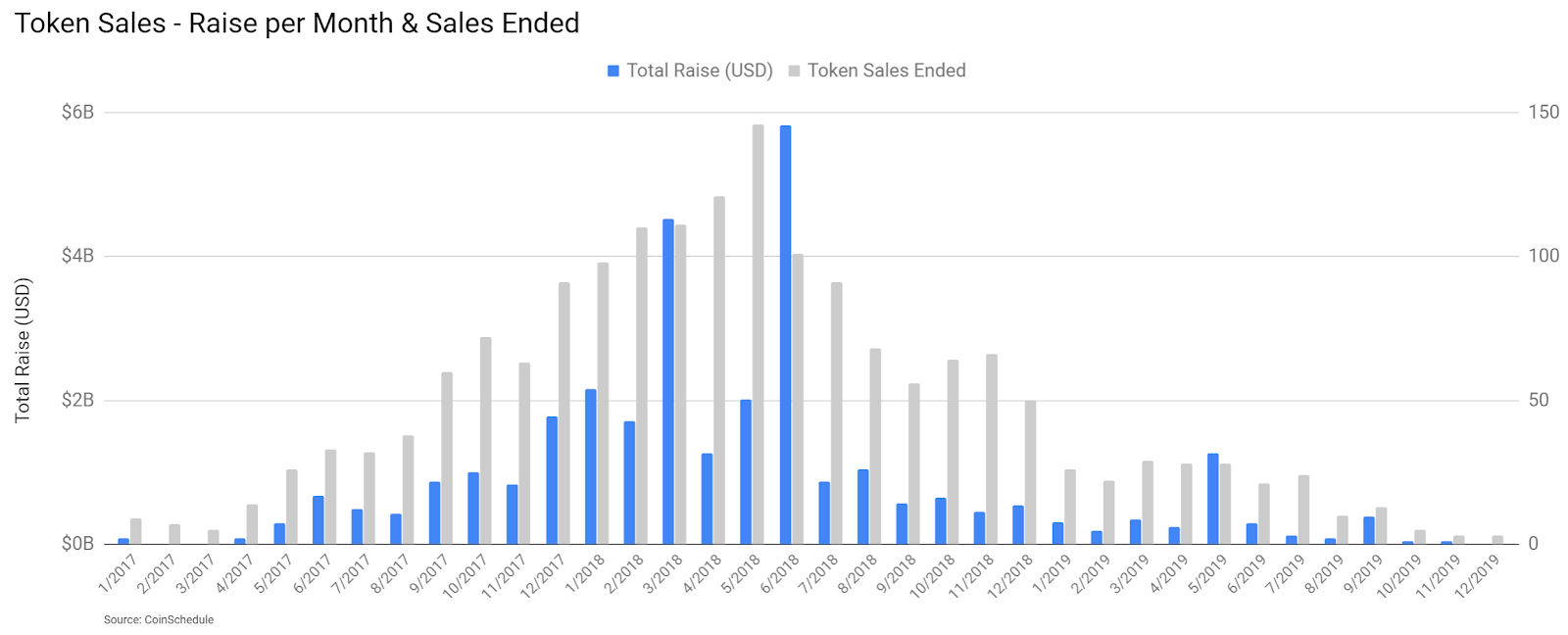

The month of May marked an almost 12 month high for ICO funding, thanks to Bitfinex’s non-ETH token raise, LEO. At the same time, Initial Exchange Offerings (IEO), where crowdsales are facilitated by an exchange, are increasing in popularity. However, these IEOs typically do not use ETH or have a native blockchain.

Globally, ICOs are increasingly moving away from public sales, likely due to fear of regulatory reproach and a shifting regulatory landscape. 2018 saw both the highest number of ICOs, at 1,075, and the largest USD sum raised in one year, at US$21.48 billion. Thus far in 2019, there have been 205 ICOs or IEOs, raising a total of just over US$3.24 billion. In contrast, the total USD raise in January 2018 was US$2.81 billion. Over 200 2018 ICOs now have a -80% return on investment.

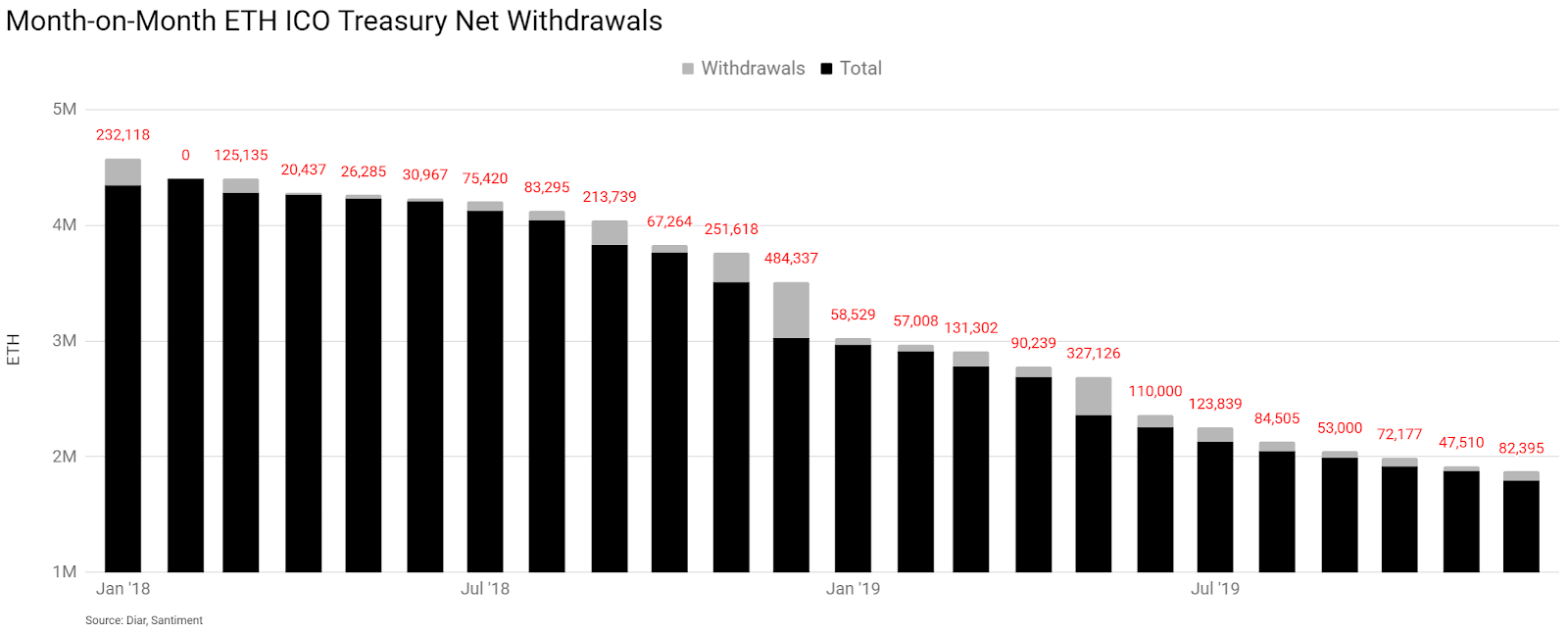

Transparent ICO treasury balances have reduced significantly throughout 2018 and 2019, both in USD value and in ETH quantity. The month of December 2018 saw the largest outflows since January 2018 at just over 484,000 ETH. May 2019 saw outflows totaling over 327,000 ETH, the largest since December. Since January 2019, ICOs have withdrawn over 1.15 million ETH and continue to hold 1.87 million ETH total.

The three largest remaining treasuries are Golem, DigixDAO, and Polkadot, at 366,380 ETH, 335,430 ETH, and 306,000 ETH, respectively. Polkadot’s funds were frozen in November 2017 when a bug was executed which deleted a code library for the Parity multi-sig wallet.

The top Ethereum based dapps over the past week, ranked by volume, continue to be led by gambling, exchange, or derivative-related dapps. The 0xUniverse dapp had the most transactions over the past week at a reported 46,100.

Overall, ETH has a considerably lower number of users and transactions compared to other dapp platforms like EOS (EOS) and Tronix (TRX), both of which have no transaction fees. In February, Twitter user Kevin Rooke pointed out that of the 1,375 ETH dapps, 86% had zero users and 93% had zero transaction volume.

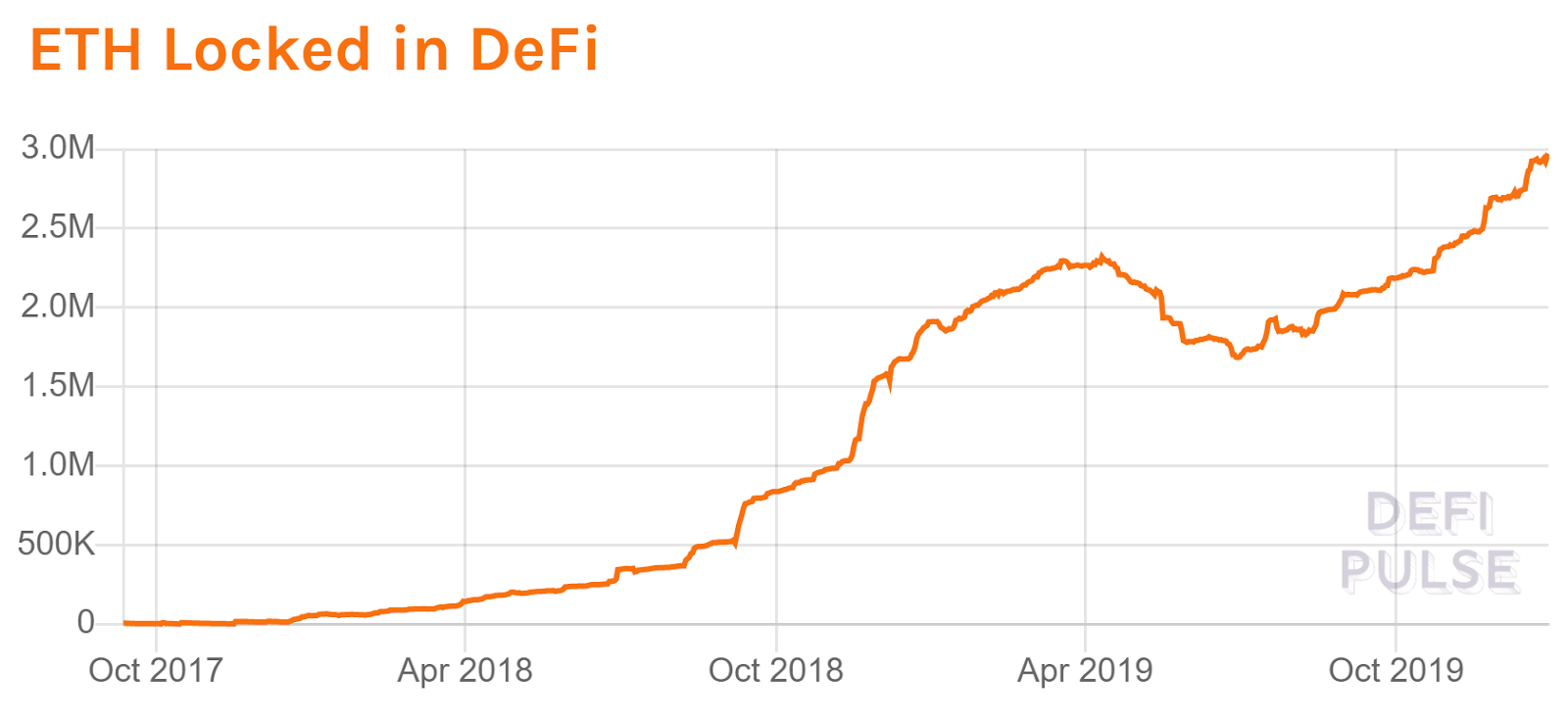

The Decentralized Finance movement, or DeFi, has increasingly gained in popularity with the total ETH held in DeFi currently at 2.95 million ETH or nearly US$700 million. Lending dapps have seen the biggest influx of money as their products began to provide a return for users. The Maker DAO, which uses collateralized debt positions to back the semi-stablecoin Dai, currently holds around 48% of all ETH in the DeFi ecosystem.

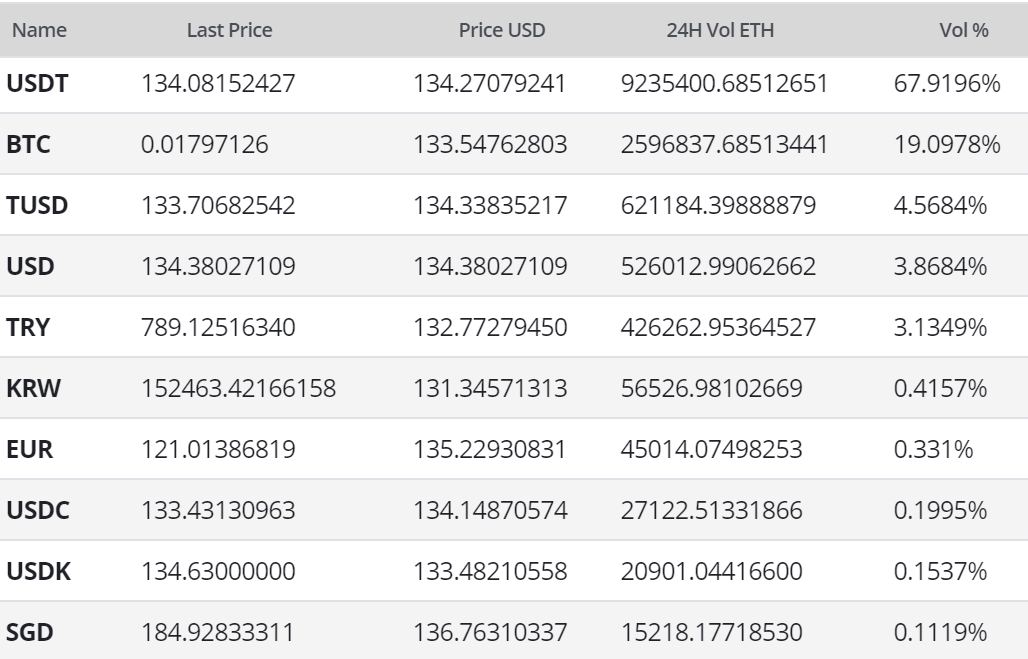

In the markets, ETH exchange-traded volume over the past 24 hours has predominantly been led by Tether (USDT) pairs. Non-USDT stablecoin volume has slowly increased over the past six months, including Dai (DAI), Paxos-Standard (PAX), Gemini-dollar (GUSD), and TrueUSD (TUSD), but continues to remain a fraction of total traded volume. A CME Group ETH futures product is also rumored to be approved sometime next year by the U.S. Commodity Futures Trading Commission.

In Asia, the Korean Won (KRW) and Yen pairs have ETH at approximately US$153. Together, both regions show relatively low interest in their fiat pairs, with nearly 0.43% of the total traded volume combined. A return of a significant premium in South Korea would signify a return to bull market conditions. Both the lack of premium and drop in trading pair percentage suggest a significant drop in retail trading on these South Korean exchanges.

Last month, the South Korean exchange Upbit reported 324,000 ETH, or about US$50 million, stolen during a cold wallet migration. Upbit has announced it will reimburse users through company funds. Over the past few years, South Korean exchanges have become a prime target for North Korean hackers, although no suspects for the most recent loss of funds are currently being released.

Worldwide Google Trends data for the term "Ethereum" spiked in July, which matched a swift increase in price. Overall, searches for “Ethereum” remain down significantly from early 2018. A slow rise in searches for "Ethereum" preceded both highs in June 2017 and January 2018, likely signaling interest from new market participants at that time. A 2015 study found a strong correlation between the Google Trends data and BTC price, while a May 2017 study concluded that when the U.S. Google "Bitcoin" searches increased dramatically, BTC price dropped.

Technical Analysis

The current ETH/USD spot price is down 91% from the all-time high set in January 2018, and down 20% from last months local high. However, the crypto asset remains up 100% from the December low late last year.

The spot price has undergone several swift reversals over the past several months, and is now essentially back to where the previous bullish move in April began. As a macro bear trend possibly emerges, roadmaps for future market movements can be found on high timeframes using Exponential Moving Averages, Volume Profile Visible Range, Pitchforks, Ichimoku Cloud, and divergences. Further background information on the technical analysis discussed below can be found here.

On the daily chart for the ETH/USD pair, the 50-day Exponential Moving Average (EMA) and 200-day EMA Death Cross occurred on August 24th, a signal for bear market conditions. Based on the Volume Profile Visible Range (VPVR - horizontal bars, chart below), the current spot price now sits below both the US$212 and US$ 140 resistance nodes. There are no bullish RSI or volume divergences at this time to suggest waning bearish momentum.

The long/short open interest on Bitfinex (top panel, chart below) is currently 91% long with long positions increasing slightly since mid-November. A significant price movement downwards will result in an exaggerated move further, as the long positions will continue to unwind. This is known as a “long squeeze.” However, Bitfinex long/short ratios have historically had little bearing on Ethereum price action.

Additionally, the spot price continues to be bound by a bearish Pitchfork (PF) with anchor points in December 2017 and April and May 2018. In April, the spot price breached the median line (yellow) to the upside, for the first time since August 2018. Upside resistance sits at US$139 with near term support at US$109. If the current market price fails to hold above support, a return to the median line at US$55 is possible within the next few weeks.

Turning to the Ichimoku Cloud, four metrics are used to indicate if a trend exists; the current price in relation to the Cloud, the color of the Cloud (red for bearish, green for bullish), the Tenkan (T) and Kijun (K) cross, and the Lagging Span. The best entry always occurs when most of the signals flip from bearish to bullish, or vice versa.

Cloud metrics on the daily time frame, with doubled settings (20/60/120/30) for more accurate signals, are bearish; price is below the Cloud, the Cloud is bearish, the TK cross is bearish, and the Lagging Span is below Cloud and near the current spot price. A traditional long entry signal will not trigger until the spot price is once again above the Cloud. However, a TK c-clamp, or TK disequilibrium, does signal the high probability of reversal to the Kijun at US$156 before further bearish momentum.

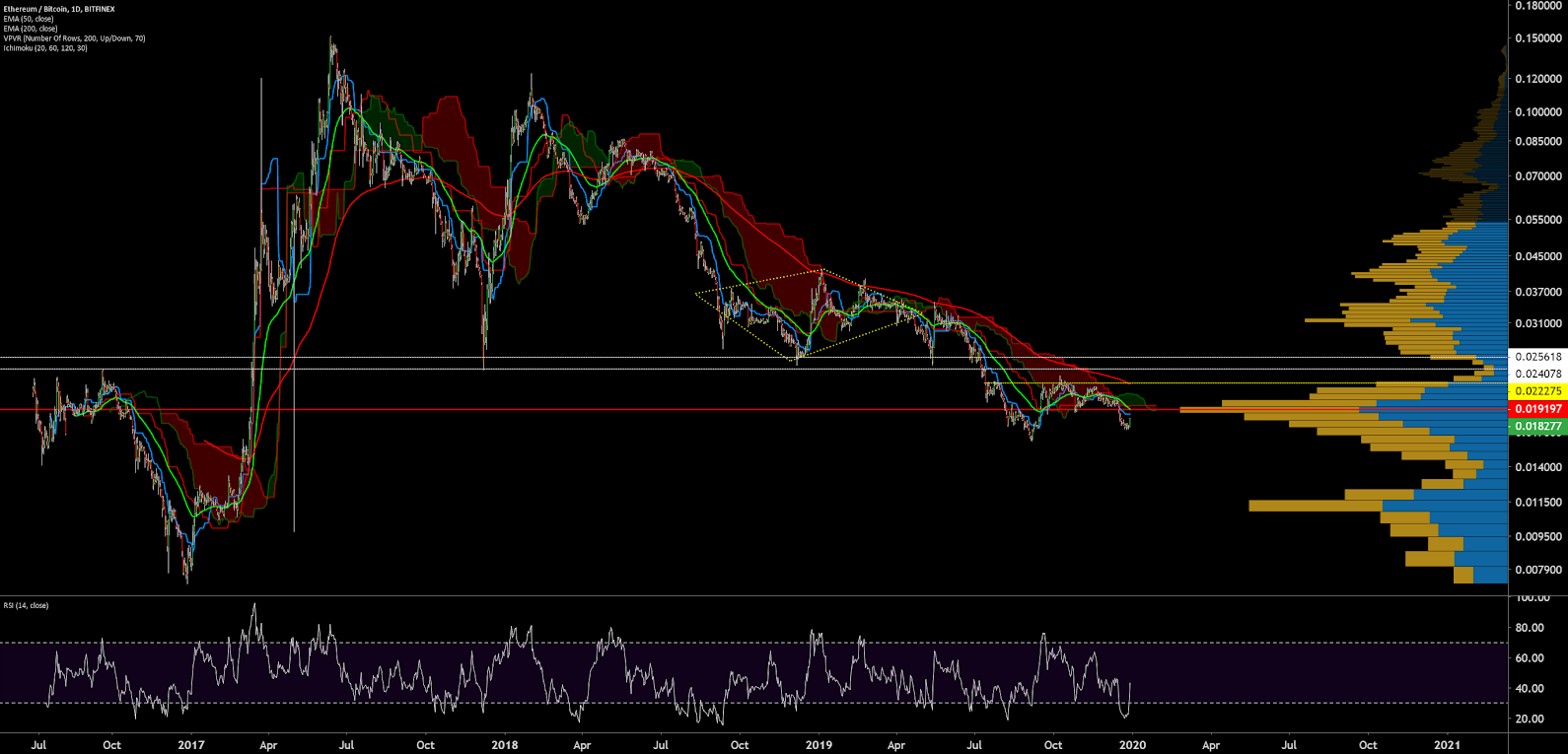

Lastly, on the daily ETH/BTC chart, trend indicators are bearish with the market currently attempting a mean reversion. The 50-day EMA and 200-day EMAs are currently bearishly crossed with the spot price last being denied at the 200-day EMA in mid-May. A continued mean reversion attempt back to the 200-day EMA, at 0.0222 BTC, is possible in the near term.

Cloud metrics using doubled settings are bearish, with a Kumo breakout below the Cloud occurring in mid-June. In the future, a bullish 50/200 EMA cross, as well as a Kumo breakout, should act as a strong buy signal for many traders. There are also no bullish or bearish divergences at this time.

Conclusion

On-chain fundamentals have been mixed over the past few months, leading into the Istanbul hard fork, which is now live on mainnet. Hash rate and transactions per day have declined to multi-month lows as a difficulty Ice Age has increased block times significantly over the past month. To remove this difficulty bomb, originally added to promote the transition from ETH 1.0 to ETH 2.0, another hard fork is set for January 2nd. The ProgPoW consensus algorithm change is likely coming in the next six months via part two of the Istanbul hard fork. Although ETH 2.0 is still in the early stages of development, the changes are actively being discussed, debated, and coded, with a phase zero release slated for January 2020.

ETH locked in DeFi apps continues to increase as ETH held by ICO treasuries continues to decrease, potentially providing a new avenue to decrease the circulating ETH supply. ICOs on the ETH chain have essentially trended to zero over the past year. As DeFi usage increases, the NVT metric may need to be retooled to better represent and include smart contract activity, such as Dai transfers.

Technicals are currently bearish for both the ETH/USD pair and ETH/BTC pair based on trend metrics. Both pairs are below the 200-day EMA and daily Cloud. ETH/USD remains held within the confines of a multi-month bearish pitchfork and below the no man’s land of US$150 - US$160. The daily ETH/USD Cloud suggests a mean reversion attempt to the Kijun at US$155 in the near term. The ETH/BTC pair is also in the midst of an active mean reversion attempt to the 200-day EMA at 0.0222 BTC.

OhNoCrypto

via https://www.ohnocrypto.com

Josh Olszewicz, Khareem Sudlow